Retirement planning is a crucial aspect of financial security, and building a substantial nest egg is essential for a comfortable retirement. This article delves into the foundational principles of retirement savings and provides strategic insights to help you grow and maintain your wealth throughout your golden years. Whether you’re just starting or looking for ways to optimize your current savings, these tips will guide you on the path to a successful retirement.

Key Takeaways

- Understanding the basics of retirement planning and the impact of compound interest is the first step towards building a secure future.

- Choosing the right retirement accounts and contributing consistently can significantly enhance your nest egg’s growth potential.

- Diversification, risk assessment, and contribution maximization are key strategies for a robust retirement portfolio.

- It’s never too late to start saving for retirement; overcoming obstacles like debt and market volatility is part of the journey.

- Transitioning from saving to spending your retirement savings requires careful planning to ensure a steady income in your later years.

Laying the Groundwork for Retirement

Understanding Retirement Planning Fundamentals

Retirement planning is a multifaceted process that encompasses more than just saving money; it’s about creating a comprehensive strategy that integrates your financial, social, and lifestyle aspirations. The foundation of a solid retirement plan is understanding the various components that contribute to a secure future.

To lay the groundwork, one must assess their current financial situation, which includes calculating net worth, reviewing income, tracking expenses, analyzing savings, and evaluating debt. This assessment is crucial as it sets the stage for informed decision-making:

- Calculate Your Net Worth

- Review Your Income

- Track Your Expenses

- Analyze Your Savings

- Evaluate Your Debt

Setting clear retirement goals is essential. Determine your desired retirement age, assess your financial readiness, and develop a plan with specific milestones. Remember, the earlier you start planning, the more time you have to grow your nest egg through the power of compound interest and strategic investments.

Understanding the different types of retirement accounts, such as Individual Retirement Accounts (IRAs), and the benefits they offer is a key step in retirement planning. Each account type has its own set of rules, advantages, and limitations, which must be navigated carefully to maximize your retirement savings.

The Role of Compound Interest in Growing Your Nest Egg

One of the most powerful tools in your retirement planning arsenal is compound interest. By starting early and saving consistently, you can harness the exponential growth potential of your investments over time. The magic of compound interest lies in its ability to increase the amount of money upon which interest is calculated each year by adding the previous period’s interest to the principal balance.

Compound interest’s effect is most potent over long periods; the earlier you start saving, the more significant the impact on your retirement savings. This is because each year’s gains build upon the previous years’, creating a snowball effect of increasing value.

Understanding the ‘Rule of 72’ can provide a quick estimate of how long it will take for your investments to double. Simply divide 72 by your annual rate of return. For instance, with a 7% return, it would take approximately 10 years for your money to double. Here’s a quick reference:

| Annual Rate of Return (%) | Years to Double |

| 4 | 18 |

| 6 | 12 |

| 8 | 9 |

| 10 | 7.2 |

Remember, the key to maximizing compound interest is to start as early as possible and to save regularly. This approach allows you to take full advantage of the growth potential of your retirement funds.

Choosing the Right Retirement Accounts

Selecting the appropriate retirement account is a pivotal decision in retirement planning. Different accounts offer varying benefits, and understanding these can significantly impact your financial readiness for retirement. Here’s a brief guide to help you navigate your options:

- 401(k)s and similar employer-sponsored plans: These plans are often accompanied by employer matching contributions, which can substantially boost your savings.

- Traditional IRAs: Contributions to these accounts may be tax-deductible, providing immediate tax benefits.

- Roth IRAs: Qualified withdrawals from these accounts are tax-free, offering long-term tax advantages.

- SEP IRAs and Solo 401(k)s: For the self-employed and small business owners, these plans allow for higher contribution limits.

It’s crucial to start saving early and to take advantage of any employer matching contributions as part of your strategy.

Remember, each type of account has its own set of rules regarding contribution limits, tax implications, and withdrawal penalties. Assess your financial situation, set specific goals, and develop a plan that aligns with your retirement age and risk tolerance.

Strategies for Building a Robust Retirement Portfolio

Diversifying Your Investment Approach

To safeguard your retirement savings, it’s crucial to diversify your investments. This strategy involves spreading your investments across various asset classes, including stocks, bonds, real estate, and commodities. Diversification can help reduce the risk of significant losses and enhance the potential for long-term growth.

By maintaining a diversified portfolio, you’re not putting all your eggs in one basket, which is essential for weathering the ups and downs of the market.

Regularly reviewing and rebalancing your portfolio is also important to ensure it stays in line with your risk tolerance and retirement objectives. Additionally, exploring tax-efficient investment strategies, such as maximizing contributions to tax-advantaged accounts, can optimize your returns.

Here’s a simple list to check when diversifying your portfolio:

- Include a mix of asset classes (stocks, bonds, real estate)

- Assess and adjust your risk tolerance

- Rebalance your portfolio periodically

- Consider tax implications and strategies

Assessing Risk and Adjusting Your Strategy Over Time

As you progress through different stages of life, your retirement plan needs to evolve. It’s crucial to conduct regular retirement checkups to ensure your savings align with your long-term goals. Here are 5 simple steps to evaluate your savings:

- Clarify your savings target to understand what you’re aiming for.

- Assess your retirement savings to see if you’re on track.

- Bump up your contributions whenever possible to maximize growth.

- Consider your tax burden and how it affects your savings.

- Rebalance your portfolio if necessary to maintain your desired risk level.

Stay Agile: Your retirement plan should be flexible enough to adapt to life’s surprises. Whether it’s a job change, a major expense, or a shift in market conditions, periodically review and adjust your retirement plan to stay on track towards your goals.

Reassessing your risk tolerance is also a key part of this process. As you age, you may find yourself gravitating towards more conservative investments to protect your nest egg. It’s important to ensure that your investment strategy is in line with your current risk tolerance and to adjust your investments accordingly.

Maximizing Contributions to Retirement Accounts

To ensure a comfortable retirement, it’s crucial to maximize your contributions to retirement accounts. Starting early and taking advantage of compounding interest can make a significant difference in the long run. If you have access to an employer-sponsored plan like a 401(k) or 403(b), prioritize contributing at least enough to receive the full employer match, as it’s akin to receiving a guaranteed return on your investment.

Harnessing the power of employer benefits is a key strategy in retirement planning. By maximizing your contributions and securing employer matches, you can accelerate the growth of your nest egg.

Understanding the contribution limits and eligibility requirements for different retirement accounts is essential. Here’s a quick overview for 2021:

- 401(k) plan: Up to $19,500

- Traditional or Roth IRA: Up to $6,000

- Catch-up contributions (if over age 50): Additional $1,000 for IRAs

Remember, these limits are subject to annual adjustments, so it’s important to stay informed and plan accordingly. For those who start saving later in life, catch-up contributions can be a valuable tool to bolster retirement savings.

Overcoming Obstacles to Retirement Savings

Addressing the Challenges of Late Starters

Starting your retirement savings later in life can be daunting, but it’s important to remember that it’s never too late to begin. For those who have delayed their retirement planning, there are still effective strategies to build a substantial nest egg.

- Maximize your 401(k) contributions to take full advantage of employer matches and tax benefits.

- Explore catch-up contributions if you’re over 50, allowing for larger annual deposits into retirement accounts.

- Prioritize high-interest debt repayment to free up more funds for saving.

- Adjust your investment portfolio to balance growth potential with risk management.

- Consider working an additional few years to boost savings and delay Social Security benefits for a higher payout.

While the journey may be challenging, every step taken is a stride towards a more secure retirement. Proactive measures and a focused approach can help late starters compensate for lost time.

Remember, the earlier you start, the more you can leverage compound interest. However, even if you’re starting later, each contribution helps you inch closer to your retirement goals. Assess your current financial situation, set realistic targets, and consult with a financial advisor to tailor a plan that suits your unique circumstances.

Managing Debt While Saving for Retirement

When preparing for retirement, it’s crucial to balance debt management with savings. Reviewing your debt is the first step; list all your obligations, from credit card balances to mortgages. This clarity allows you to prioritize repayments, focusing on high-interest debts first to alleviate financial pressure.

- Prioritize high-interest debt: Pay off credit cards and loans with the highest rates first.

- Create a budget: Track income and expenses to find opportunities for savings.

- Build an emergency fund: Aim for 3-6 months of living expenses to avoid new debt.

- Consult a professional: A financial advisor can tailor a debt management plan.

Balancing debt repayment with retirement contributions is a delicate act. An effective strategy is to allocate funds to both, ensuring you’re not sacrificing your future comfort for present obligations. Remember, the sooner you control your debt, the more you can contribute to your retirement savings, benefiting from compound interest over time.

Dealing with Market Volatility and Economic Uncertainty

Market volatility and economic uncertainty can be daunting for those saving for retirement. Diversifying your investment portfolio is a key strategy to mitigate these risks. By spreading investments across various asset classes, such as stocks, bonds, and real estate, you can reduce the impact of a downturn in any single sector on your overall portfolio.

Rebalancing your portfolio regularly is also crucial. This practice ensures that your asset allocation remains aligned with your risk tolerance and financial goals, especially important in volatile markets. Here’s a simple guide to consider:

- Assess your risk tolerance: Understand how much volatility you can comfortably handle.

- Set clear financial goals: Define what you aim to achieve with your retirement savings.

- Rebalance regularly: Adjust your investments to maintain your desired asset allocation.

Remember, while no investment strategy can guarantee against loss, being proactive and prepared can help protect your retirement savings from market fluctuations. It’s essential to have a solid investment plan in place before a downturn occurs to weather the storm more effectively.

Transitioning from Accumulation to Distribution

Understanding Withdrawal Strategies and Risks

When transitioning from saving to spending your retirement funds, it’s crucial to develop a withdrawal strategy that ensures your nest egg lasts throughout your retirement years. Factors such as your desired lifestyle, longevity risk, and tax implications play a significant role in determining an appropriate withdrawal rate.

It’s essential to explore various income sources beyond traditional pensions and Social Security. Options like annuities, rental income, and part-time work can supplement your retirement income, providing additional financial security.

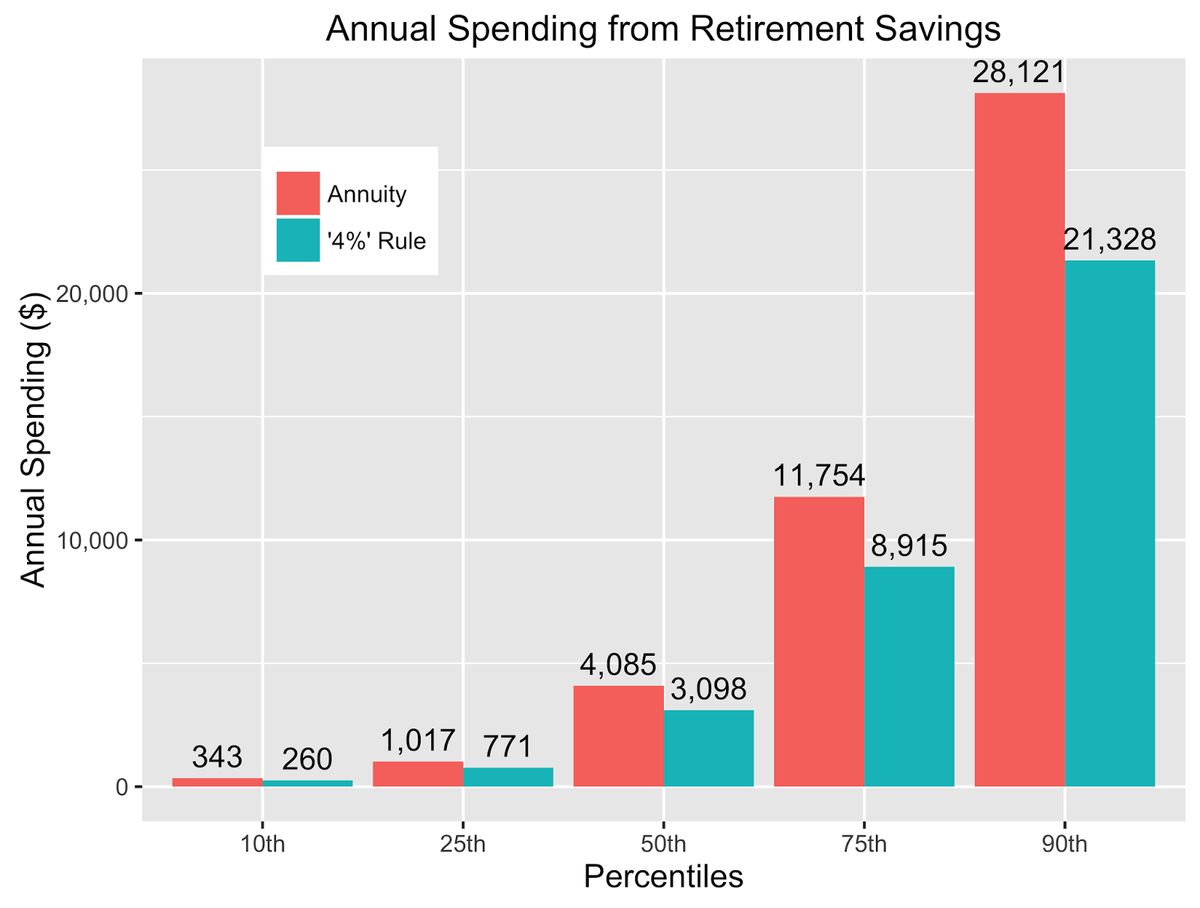

The 4% rule is a commonly referenced guideline suggesting that withdrawing 4% of your retirement savings annually is a safe rate to prevent depleting your funds. However, this rule is not one-size-fits-all; market volatility and personal circumstances may necessitate adjustments.

Systematic withdrawal plans offer a structured approach, allowing retirees to withdraw fixed amounts at regular intervals. This method helps manage cash flow and can contribute to the longevity of your savings. Remember, the sequence of withdrawal risk is a critical consideration, especially during market downturns early in retirement.

Ensuring a Steady Retirement Income

To maintain financial stability in retirement, it’s crucial to have a steady stream of income that can cover living expenses and adapt to inflation. Diversifying income sources is a key strategy to achieve this goal. By combining different income streams, retirees can better manage risks and ensure that their savings last throughout retirement.

One widely recognized guideline for withdrawal rates is the 4% rule, which suggests that retirees should withdraw no more than 4% of their savings each year to maintain a safe, steady stream of income. This approach can help prevent the depletion of retirement funds too early.

When exploring retirement income options, consider the following: Annuities for guaranteed income Systematic withdrawal plans to manage savings Dividend-paying stocks for potential growth Rental properties for passive income Part-time employment to supplement retirement income

It’s also important to regularly review and adjust your retirement plan as you age, taking into account changes in your health, life expectancy, and the economic environment.

Exploring Annuities and Other Income Solutions

When planning for retirement, ensuring a steady income stream is paramount. Annuities offer a guaranteed income, providing financial security regardless of market conditions. It’s crucial to choose a reputable provider and be wary of high fees that can erode your returns. Shopping around for the best annuity is a key step in retirement planning.

Beyond annuities, there are other income solutions to consider:

- Systematic Withdrawal Plans

- Dividend-Paying Stocks

- Rental Properties

- Part-Time Employment

Each option has its own set of advantages and considerations. For instance, systematic withdrawal plans allow for flexibility in how much you withdraw each year, while dividend-paying stocks can offer growth potential and income. Rental properties provide a tangible asset that can generate regular income, and part-time employment can supplement retirement savings while keeping retirees active.

Secure retirement income solutions are essential for peace of mind, especially during market fluctuations. They help maintain your lifestyle and ensure that your nest egg lasts throughout your retirement years.

Maintaining Your Nest Egg in Retirement

Adjusting Your Lifestyle to Preserve Savings

As you transition into retirement, adjusting your lifestyle to preserve your savings becomes crucial. It’s about finding a balance between enjoying your golden years and ensuring your nest egg lasts. Consider the following points:

- Evaluate your spending habits and cut back on non-essential expenses.

- Prioritize your financial goals and align your spending accordingly.

- Stay agile and be prepared to adjust your plan as life circumstances evolve.

Making adjustments to your lifestyle isn’t just about cutting costs; it’s about optimizing your spending to support a sustainable retirement.

Remember, retirement planning is not a set-it-and-forget-it endeavor. Periodically review your retirement plan to stay on track towards your goals. If your expenses exceed your income, consider reducing expenses, finding additional income sources, or adjusting your investment strategy.

Healthcare Considerations and Costs

As you transition into retirement, prioritize healthcare planning to protect your nest egg from potential medical expenses. The U.S. Department of Health and Human Services reports that a substantial number of retirees will require long-term care services, making it crucial to prepare for these costs.

- Evaluate your health and longevity to determine if you need to allocate more funds for healthcare.

- Ensure you have adequate health insurance coverage, including Medicare and supplemental insurance.

- Consider long-term care insurance to cover expenses of assisted living or nursing home care.

By planning for healthcare expenses and long-term care, you can safeguard your financial future and maintain peace of mind during your retirement years.

Remember, the average annual cost of a private room in a nursing home was over $100,000 in 2020. Planning for long-term care is essential to prevent your retirement savings from being depleted by high healthcare costs.

Navigating Taxes and Inflation in Retirement

Inflation can significantly diminish the value of your retirement savings, making it crucial to adopt strategies that counteract its effects. To protect against inflation, consider diversifying your portfolio with assets that historically perform well during inflationary periods, such as stocks, real estate, and commodities. Additionally, Treasury Inflation-Protected Securities (TIPS) can offer a return that keeps pace with inflation.

When planning for retirement, it’s essential to understand how taxes will impact your income. Structuring your withdrawals to minimize tax liability can help preserve your nest egg. For instance, knowing when to withdraw from tax-deferred accounts versus Roth accounts can make a significant difference in your after-tax income.

Adequate insurance coverage is also a key component in safeguarding your retirement finances. It can help manage unexpected costs and provide peace of mind. Remember, the only remedy to inflation in retirement is to save early and often if you can.

Conclusion

As we’ve explored throughout this article, building a substantial retirement nest egg is a multifaceted endeavor that requires early planning, consistent saving, and strategic investing. Whether you’re just starting out or looking to optimize your existing savings, understanding the power of compound interest, the types of retirement accounts available, and the risks involved in spending down your nest egg are crucial. Remember, it’s never too late to start or to refine your approach. By setting clear retirement goals, assessing your financial situation, and considering various income options like annuities or rental properties, you can navigate the challenges of retirement planning. Stay informed, seek advice when needed, and take proactive steps towards securing your financial future. Retirement may seem distant, but the actions you take today will pave the way for a comfortable and fulfilling retirement.

FAQs

Retirement planning involves setting retirement goals, assessing your current financial situation, estimating retirement expenses, and creating a savings plan to ensure you have a steady income after you retire.

Compound interest is the interest you earn on both your initial principal and the accumulated interest from previous periods. Over time, this compounding effect can significantly increase the value of your retirement savings, especially if you start early.

Common types of retirement accounts include 401(k)s, Individual Retirement Accounts (IRAs), and Health Savings Accounts (HSAs), each with different tax advantages and contribution limits. Choosing the right mix depends on your financial situation and retirement goals.

Diversifying your portfolio involves spreading your investments across different asset classes, such as stocks, bonds, and real estate, to reduce risk and improve potential returns. This can be achieved through mutual funds, exchange-traded funds (ETFs), and other investment vehicles.

Late starters can catch up by maximizing their retirement account contributions, possibly taking advantage of catch-up contributions if they’re over 50, reducing expenses to free up more money for savings, and considering working longer to delay tapping into retirement funds.

To convert savings into income, you can consider various withdrawal strategies, such as the systematic withdrawal plan, purchasing annuities for guaranteed income, investing in dividend-paying stocks, or generating income through rental properties or part-time work.