Navigating the complexities of credit scores is essential for financial health. This article, ‘Credit Score Fundamentals,’ aims to demystify the elements that constitute a credit score, outline strategies for improvement, clarify how scores are calculated, dispel common myths, and provide guidance for strategic financial planning. With the right knowledge and actions, individuals can enhance their creditworthiness and secure a better financial future.

Key Takeaways

- Understanding the five core components of credit scores (payment history, credit utilization, credit history length, credit mix, and new credit inquiries) is crucial for credit management.

- Responsible credit behavior, such as timely payments and maintaining low debt levels, positively influences your credit score over time.

- Credit scores are calculated based on a model that emphasizes payment history and credit utilization, among other factors, and it’s important to know where you stand within the credit score ranges.

- Several myths surrounding credit scores persist, but knowing the facts, such as the harmless nature of self-credit checks, can help maintain a realistic approach to credit management.

- Strategic financial planning, including regular credit monitoring and understanding your financial habits, is key to long-term credit score improvement.

Understanding Credit Score Components

The Role of Payment History

Your payment history is a critical factor in determining your credit score, accounting for a significant portion of the calculation. It reflects your reliability in paying back debts on time and is a key indicator of creditworthiness to lenders. A consistent record of timely payments can lead to more favorable loan terms and interest rates.

Maintaining a positive payment history is not only beneficial for your credit score but also for your overall financial health. It can be the gateway to better financial opportunities and a reflection of your financial responsibility.

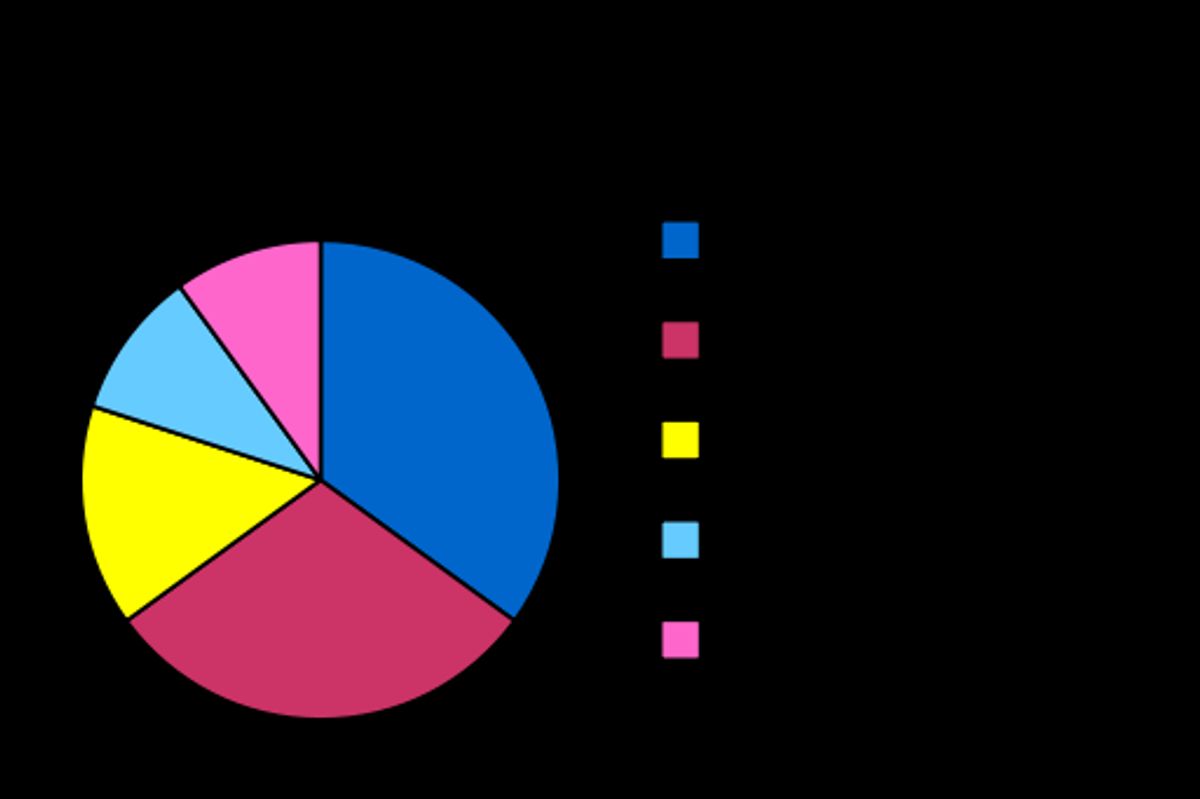

Here is a breakdown of the components that influence your credit score:

- Payment history (35%)

- Amount owed (30%)

- Length of credit history (15%)

- New credit (10%)

- Credit mix (10%)

Experts like Sellery emphasize the importance of never missing a minimum payment. Automating this process can ensure that payments are made on time, which is especially crucial for those working to rebuild their credit.

Credit Utilization and Its Impact

Credit utilization refers to the ratio of your credit card balances to your credit limits. It is a pivotal component in the calculation of your credit score. Keeping your utilization below 30% is considered a sign of prudent credit management and can positively influence your score.

- High Utilization (>30%): May indicate over-reliance on credit and can lower your score.

- Moderate Utilization (10-30%): Shows responsible credit use and can boost your score.

- Low Utilization (<10%): Demonstrates excellent credit control, potentially increasing your score.

Credit utilization is a dynamic factor; even if you pay off your balances in full each month, high utilization at any point in the billing cycle can affect your score.

Misconceptions about credit utilization can lead to counterproductive behaviors, such as maxing out credit cards to demonstrate reliability. However, this strategy often backfires, as credit rating agencies favor utilization levels around a third of the available credit. Regular monitoring and responsible credit card use are key to managing this aspect of your credit score.

The Importance of Credit History Length

The length of your credit history is a significant factor in the credit scoring process, accounting for about 15% of your FICO score. A longer credit history can provide a more accurate representation of your financial habits and reliability.

- Expand the scope of your credit history to strengthen your credit score foundation.

- It’s advisable to apply for credit occasionally; too many hard inquiries can negatively impact your score.

Lenders value a track record of prudent credit management. A lengthy credit history suggests responsible credit use over time, which can lead to a more favorable credit score. However, it’s not just about the age of your accounts but also how consistently you’ve managed credit throughout that time.

Maintaining older credit accounts can be beneficial, as they contribute to the average age of your credit history. Closing old accounts might shorten your credit history and potentially lower your score.

Diversifying Credit Mix

A well-rounded credit portfolio is essential for demonstrating your financial acumen. Blend different types of credit, such as credit cards, personal loans, and mortgages, to show lenders your capability to manage diverse financial obligations. A mix of both secured and unsecured debts is often viewed favorably by banks, as it reflects a responsible borrowing behavior.

When evaluating your creditworthiness, lenders and credit bureaus look for a variety of credit accounts in your history. This variety, known as your credit mix, can positively influence your credit score.

However, it’s important to approach credit diversification strategically. Rapidly acquiring multiple lines of credit can be detrimental to your rating. Instead, consider the following steps to enhance your credit mix:

- Evaluate Your Credit Mix: Review your credit report to see the types of accounts you currently have open.

- Strategic Use of Credit: When considering new credit, think about how it fits into your overall financial picture.

- Balance Secured and Unsecured Loans: Aim for a healthy balance between secured loans (like car or home loans) and unsecured loans (like personal loans).

The Effect of New Credit Inquiries

Every time you apply for a new line of credit, a hard inquiry is recorded on your credit report. These inquiries signal to potential lenders that you are seeking additional credit, which can be interpreted as a higher risk, especially if there are many inquiries in a short period. Hard inquiries can remain on your credit report for up to two years, although their impact on your credit score diminishes over time.

While a single inquiry may only slightly affect your credit score, multiple inquiries in a short timeframe can have a more significant effect. It’s crucial to be strategic about when and how often you apply for new credit.

Here’s a quick overview of how different types of credit inquiries affect your score:

- Soft inquiries: These do not affect your credit score and include background checks, pre-qualified credit offers, and your own credit checks.

- Hard inquiries: These occur when a financial institution checks your credit for lending purposes and can affect your score.

Remember, when shopping for an auto loan or mortgage, multiple inquiries within a short period are typically treated as a single inquiry to allow for rate shopping without damaging your credit score excessively.

Improving Your Credit Score Responsibly

Timely Bill Payments

Making timely bill payments is one of the most effective ways to ensure a healthy credit score. Each on-time payment is a positive mark on your credit history, demonstrating your financial responsibility to lenders.

- Set up automatic payments to avoid missing due dates.

- Prioritize minimum payments to keep accounts in good standing.

- Communicate with creditors if you anticipate payment difficulties.

Timely payments contribute significantly to your credit score, showcasing your reliability. It’s not just about avoiding late fees; it’s about building a track record of trustworthiness.

Remember, even one late payment can have a detrimental effect on your credit score. With an open form of credit, when any amount is left unpaid after the due date, the account is immediately considered not only overdue, but over-limit as well. It’s essential to stay organized and proactive in managing your bills to maintain and improve your credit standing.

Managing Debt Levels

Effectively managing debt levels is crucial for maintaining and improving your credit score. It’s important to approach your bank for assistance if you’re struggling with EMIs, as they may help restructure your debt. Keeping your debt-to-credit ratio below 30% is a key strategy, as high utilization can negatively impact your score.

Paying more than the minimum on your credit cards and avoiding maxing out your limits are practical steps towards debt management.

Consolidating your debts into a single payment can simplify your finances and may lead to lower interest rates. Remember to periodically request your free credit report to check for inaccuracies or fraud. Here’s a simple action plan to manage your debt levels:

- Approach your bank for debt restructuring if needed.

- Aim to keep your debt-to-credit ratio under 30%.

- Pay more than the minimum amount due on credit cards.

- Consider debt consolidation for easier management and potential interest savings.

- Regularly review your credit report for errors or fraudulent activity.

Avoiding Excessive Credit Applications

When it comes to maintaining a healthy credit score, avoiding excessive credit applications is crucial. Each time you apply for credit, a hard inquiry is made on your credit report, which can temporarily lower your score. It’s important to be strategic about when and how often you apply for new credit lines.

- Soft pulls, such as checking your own credit score, do not impact your credit. These can be done frequently and without worry.

- Hard pulls, on the other hand, are conducted by lenders when you apply for credit and can affect your score. Limit these to necessary applications only.

Be mindful that credit bureaus may interpret frequent credit applications as a sign of financial distress. This perception can negatively impact your credit score, even if you’re simply shopping for the best rates.

Remember, not all credit is created equal. Secured credit cards, for example, can be a safer option as they require a cash deposit and can help build credit without the risk of overextending. Balance your credit utilization and avoid reaching your credit limit to keep your financial health in check.

Consistency in Financial Behavior

Maintaining a consistent financial behavior is crucial for a healthy credit score. Regular and timely payments are not just about avoiding late fees; they signal to creditors your dependability as a borrower. This consistency extends beyond just bill payments to the overall management of your finances, including the use of credit.

- Set up automatic payments to avoid missed due dates.

- Keep a steady employment history, as lenders may consider this.

- Regularly review your financial habits and adjust as needed.

Consistency in your financial behavior demonstrates to lenders a stable and predictable financial pattern, which can positively influence your credit score over time.

Remember, while occasional mishaps may not severely harm your credit score, a pattern of erratic financial behavior can raise red flags with lenders. It’s the cumulative effect of your financial decisions that shapes your creditworthiness.

Monitoring Credit Regularly

Regularly monitoring your credit is a critical step in managing your financial health. By keeping a close eye on your credit report, you can quickly identify any inaccuracies or signs of fraud. This proactive approach allows you to address issues before they escalate, potentially saving you from future headaches and financial setbacks.

- Request your free credit report periodically to check for errors.

- Stay informed about changes in your credit score as it is recalculated every month.

- Keep your personal information up to date with all credit bureaus.

Regular credit monitoring empowers you to take immediate action if something is amiss, ensuring that your credit score remains an accurate reflection of your financial responsibility.

The Calculation of Credit Scores

Understanding the Credit Scoring Model

Credit scoring models are complex systems used by lenders to evaluate an individual’s creditworthiness. Banks usually grant loans based on a credit scoring model that combines qualitative and quantitative analysis. These models are designed to predict the likelihood of a borrower defaulting on a loan by analyzing various aspects of their financial history.

The formula for credit score calculation can vary, but common factors include:

- Payment history

- Amount owed

- Length of credit history

- New credit

- Credit mix

Credit scores are determined without considering salary, focusing instead on credit behavior rather than income.

Understanding these components is crucial for interpreting your credit report accurately and for taking steps to improve your score. Each credit bureau may have its proprietary process for computing credit scores, but the core elements remain consistent across different models.

Factors Influencing Credit Score Calculation

Understanding the factors that influence your credit score is essential for maintaining or improving your financial health. The credit scoring models used by bureaus assess a range of elements to determine your score.

- Payment history is the most significant component, accounting for 35% of your score. It reflects whether you make payments on time.

- The amount owed, or credit utilization, makes up 30% and is a measure of how much credit you’re using compared to your limits.

- Length of credit history contributes 15%, with longer credit histories generally being seen as more favorable.

- New credit and the number of inquiries account for 10%, indicating how often you apply for new credit.

- Lastly, the credit mix—the types of credit accounts you have—also makes up 10% of your score.

It’s important to note that income does not directly affect your credit score; rather, it’s your credit behavior that’s evaluated.

Each of these factors plays a part in the complex algorithm that calculates your credit score. While some factors weigh more heavily than others, a balanced approach to credit management is key to a healthy credit profile.

Interpreting Your Credit Report

Interpreting your credit report is a critical step in managing your financial health. Understanding the various sections and what they signify can empower you to make informed decisions about your credit. Here’s a simple guide to help you decode the report:

- Personal Information: Verify your name, address, and employment details are accurate.

- Credit Accounts: Review the list of your accounts, including loans and credit cards, along with their statuses.

- Credit Inquiries: Note the number of hard inquiries, as these can affect your score.

- Public Records: Check for any legal matters that may impact your credit, such as bankruptcies or liens.

- Credit Summary: This section provides a snapshot of your credit health, including total debt and available credit.

It’s essential to scrutinize each entry for accuracy. Discrepancies can be disputed with the credit bureau, which is obliged to investigate and rectify any verified errors. Regularly reviewing your credit report can also alert you to potential identity theft or fraud.

Remember, your credit report is a reflection of your financial behavior. It’s not just about the numbers; it’s about the story they tell. A good score, as defined by FICO, falls between 670 to 739. However, lenders may have their own criteria for what constitutes good credit. Stay proactive in understanding and improving your credit score for a healthier financial future.

Credit Score Ranges and What They Mean

Understanding the range into which your credit score falls is crucial for grasping how lenders view your creditworthiness. Credit scores typically range from 300 to 850, with various categories that can impact your ability to borrow and the terms you receive. Here’s a quick breakdown of the general credit score ranges:

| Range | Category |

| 300 – 579 | Poor |

| 580 – 669 | Fair |

| 670 – 739 | Good |

| 740 – 799 | Very Good |

| 800 – 850 | Excellent |

A higher credit score indicates a borrower’s dependability and a lower risk for lenders, which can lead to more favorable loan terms and interest rates.

It’s important to note that these ranges are not absolute and can vary slightly between different credit scoring models, such as FICO and VantageScore. Regardless of the model, maintaining a score in the higher ranges is generally beneficial. By understanding where you stand, you can better assess your financial health and work towards improving your score if necessary.

Common Misconceptions About Credit Scoring

When it comes to credit scoring, myths can be as pervasive as the truth. One common misconception is that applying for new credit signals financial distress, leading to a negative impact on your score. However, this is not always the case; credit inquiries can have a minimal effect if managed wisely.

Another area of confusion lies in credit utilization. Some individuals believe that maxing out credit cards and promptly paying them off demonstrates reliability. In reality, credit rating agencies favor the use of roughly one-third of your available credit. Overextending can be seen as a risk, not a sign of financial acumen.

It’s essential to approach credit with a balanced perspective, recognizing that while credit scores are important, they are not the sole indicator of financial health.

Misunderstandings can lead to counterproductive behaviors, such as the belief that constantly using up to your credit limit reflects positively on your creditworthiness. It’s crucial to dispel these myths and focus on building a strong financial foundation for a healthy credit score.

Credit Score Myths and Realities

The Obsession with Perfect Credit

In the pursuit of financial health, a perfect credit score has become a coveted goal for many. However, an overemphasis on achieving the highest score possible can overshadow the importance of maintaining overall good financial habits. A credit score is a reflection of one’s financial behavior over time, and while it’s a useful metric, it’s not the sole indicator of financial stability.

The quest for a perfect credit score should not lead to financial decisions that are counterproductive in the long run. It’s essential to remember that credit scores evolve with your financial habits, and a healthy financial routine will naturally foster a strong credit score.

Understanding that credit scores are designed to be dynamic can alleviate the pressure of perfection. Here are some key points to consider:

- A high credit score is beneficial, but not at the expense of financial well-being.

- Good spending and debt repayment habits are foundational to a healthy credit score.

- Credit scores will gradually improve as you consistently demonstrate financial responsibility.

Ultimately, a balanced approach to credit management, one that prioritizes sound financial practices, is more sustainable than fixating on a perfect score.

Myth: Checking Your Own Credit Hurts Your Score

One of the most persistent myths about credit scores is that checking your own credit report can harm your score. This is simply not true. Checking your own credit score is a soft inquiry, which has no impact on your credit score. In contrast, hard inquiries, such as those made by lenders when you apply for a loan or credit card, can affect your score if they occur frequently.

- Soft inquiries – Include personal credit checks and pre-approval offers; do not affect your score.

- Hard inquiries – Include credit applications; may affect your score if numerous.

It’s important to understand the difference between these two types of credit pulls. Regularly monitoring your credit is a responsible financial behavior and can help you catch errors or fraudulent activity early on. Remember, you can check your score as often as you like without any negative consequences.

By dispelling this myth, you can take control of your credit health by staying informed and proactive about your credit status without fear of damaging your score.

Reality: Improvements Take Time

Improving your credit score is a process that requires both consistent effort and patience. It’s crucial to understand that while positive changes, such as on-time payments, can influence your score, they do so gradually over time. A single month of positive payment history is beneficial, but a sustained period of six to twelve months is significantly more impactful in demonstrating your creditworthiness.

Establishing a solid track record of financial responsibility is essential. This means not only making payments on time but also being mindful of other factors such as credit utilization and the diversity of your credit accounts.

Remember, there are no quick fixes when it comes to credit scores. It’s a marathon, not a sprint, and taking shortcuts can often lead to setbacks. For example, applying for new credit can signal to credit bureaus that you may be in a financial crisis, which could negatively affect your score. Instead, focus on the long-term goal of building a strong credit foundation.

The Impact of Financial Crises on Credit Scores

Financial crises can lead to a turbulent period for credit scores. During such times, individuals may face challenges in maintaining their creditworthiness due to job loss, reduced income, or increased debt. This can result in a migration of borrowers across credit score categories, particularly affecting those in the subprime rate category.

It’s essential to navigate financial crises with caution to minimize the impact on your credit score. Strategic financial decisions during these times are more critical than ever.

The following points outline the typical effects of financial crises on credit scores:

- Increased likelihood of missed payments or defaults

- Potential for higher credit utilization due to reliance on credit for everyday expenses

- Difficulty in obtaining new credit, as lenders may view applications as signs of financial distress

- Long-term effects on credit history, as delinquencies and defaults can remain on credit reports for years

Understanding these impacts can help individuals prepare for and mitigate the negative consequences on their credit scores.

Separating Fact from Fiction in Credit Reporting

In the realm of credit reporting, misconceptions can lead to unnecessary anxiety and misguided decisions. Understanding the difference between myth and reality is crucial for maintaining a healthy credit profile.

- Myth: Applying for new credit signals financial crisis.

- Reality: Responsible credit applications reflect normal financial activity.

- Myth: Business credit with Experian and Equifax requires an application.

- Reality: These bureaus automatically create credit files from lender reports and public records.

It’s essential to focus on solid financial habits rather than an obsession with credit scores. Good spending and debt repayment behaviors will naturally improve your credit score over time.

Changes in credit scoring models and reporting practices, such as the proposed shift from ‘tri-merge’ to ‘bi-merge’ credit reports, are often misunderstood. Keeping informed about these developments is key to demystifying credit scores and making informed financial decisions.

Strategic Financial Planning for Better Credit

Analyzing Your Financial DNA

Understanding your financial DNA is crucial for credit score improvement. It involves a deep dive into your credit report, which acts as a financial report card, revealing your habits and areas that need attention. Platforms like CIBIL offer free annual credit reports, which are essential tools for this analysis.

To begin, list down the key components of your financial behavior:

- Review your credit report thoroughly

- Identify patterns in your spending and payment habits

- Recognize the types of credit you use and how often

- Assess your debt management strategies

By analyzing these aspects, you can pinpoint the strengths and weaknesses in your financial profile. This self-awareness is the first step towards crafting a personalized plan for credit score enhancement.

Remember, improving your credit score is a gradual process that requires consistent effort and responsible financial habits. While some changes may take effect immediately, others will manifest over time as you maintain good financial practices.

The Role of Free Credit Reports

Access to free credit reports is a cornerstone of maintaining a healthy financial profile. Regularly reviewing your credit report can reveal errors or fraudulent activity that may be affecting your credit score. It’s recommended to check your credit reports from each of the three major credit bureaus—Equifax, Experian, and TransUnion—at least once a year.

By proactively managing your credit through these reports, you can ensure that your credit history is accurately represented, which is crucial for future financial endeavors.

Understanding the details of your credit report is just as important as obtaining it. Here’s a simple breakdown of what to look for:

- Personal information accuracy

- Account histories

- Credit inquiries

- Public records

- Collections

Each section of your credit report holds significant weight in your overall credit health. Spotting discrepancies early can save you from potential headaches down the line. Remember, checking your own credit score is a soft pull that does not impact your score, so you can do this as often as necessary without worry.

Balancing Credit Management

Achieving a balance in credit management is essential for maintaining a healthy credit score. Properly managing your credit utilization ratio is a key aspect of this balance. It is recommended to keep your credit utilization below 30% to avoid negatively impacting your score. This can be done by spreading your expenses across multiple cards and ensuring that no single card is maxed out.

Diversifying your credit portfolio is also important. Including a variety of credit types, such as credit cards, loans, and a mix of secured and unsecured debts, demonstrates your capability to handle different financial obligations. However, be cautious of having too many unsecured loans, as this can be viewed unfavorably by lenders.

Balancing credit management involves a strategic approach to using and paying off credit. By maintaining low balances and a diverse credit mix, you can show lenders that you are a responsible borrower.

Remember, while it’s tempting to try and showcase reliability by maxing out a card and paying it back quickly, this strategy can backfire. Credit rating agencies prefer to see only a portion of the available credit utilized, reinforcing the importance of moderation in credit use.

Long-Term Strategies for Credit Improvement

Developing a robust strategy for long-term credit improvement involves a comprehensive approach to financial management. Consistent, responsible behavior is the cornerstone of building a better credit score over time.

- Pay credit card balances strategically to optimize your debt-to-credit ratio, aiming to keep it below 30%.

- Lengthen your credit history by maintaining older accounts and avoiding new credit unless necessary.

- Regularly monitor your credit report for errors and dispute any inaccuracies promptly.

By focusing on these long-term strategies, you can gradually enhance your creditworthiness and potentially secure more favorable borrowing terms in the future.

Remember, while there are numerous ways to boost your score, such as secured credit cards or becoming an authorized user on another’s account, the most effective methods are those that demonstrate financial prudence and stability.

Educational Resources for Credit Score Mastery

Mastering your credit score is a continuous learning process. NerdWallet offers a free credit score and tools like credit score simulators, which can be invaluable for understanding the potential impact of financial decisions on your credit standing.

To truly excel in managing your credit, it’s essential to engage with educational resources that provide actionable insights and strategies.

Here are some key resources to consider:

- Webinars led by credit experts that outline effective credit management techniques.

- Annual free credit reports from platforms like CIBIL to analyze and improve your financial habits.

- Online guides covering credit card basics, application processes, and debt management.

By utilizing these resources, you can gain a deeper comprehension of credit score dynamics and develop a robust strategy for credit improvement.

Conclusion

In conclusion, mastering the fundamentals of credit scores is essential for financial health and planning for the future. Understanding the impact of payment history, credit utilization, credit mix, and the length of credit history can empower individuals to make informed decisions and improve their creditworthiness. While it’s important to be aware of your credit score, it’s equally crucial to focus on the underlying financial habits that contribute to it. Remember, building a strong credit score is a gradual process that requires patience, discipline, and a balanced approach to credit management. By adhering to these principles, you can ensure a robust financial foundation that will serve you well in all your borrowing endeavors.

FAQs

The five main components of a credit score are payment history, credit utilization, length of credit history, credit mix, and new credit inquiries.

You can improve your credit score by making timely bill payments, managing debt levels, avoiding excessive credit applications, maintaining consistency in financial behavior, and monitoring your credit regularly.

No, checking your own credit score is considered a soft inquiry and does not affect your credit score.

Improvements in credit scores take time and depend on various factors, but consistently applying good credit habits can lead to positive changes over time.

Yes, financial crises can impact your credit score, especially if they result in missed payments or increased credit utilization.

You can find educational resources through credit bureaus, financial education platforms, and annual free credit report services like CIBIL to understand and improve your credit score.